How to Build the Amazon of Game Companies

Today at $1.3T in market capitalization, Amazon is the most valuable company in the world. Further, the company has arguably the highest defensive barriers to its business than any other company in the world.

However, when we look at gaming companies, we don’t see the same level of defensibility that we see for companies in other industries. There is no FAANG-like (Facebook, Apple, Amazon, Netflix, and Google) company in gaming with the associated massive defensive moat and confidence in long-term durability and resilience.

In gaming, we have, on the flip side, seen how once mighty game companies that were once viewed as FAANG-like companies — Machine Zone, Zynga, Kabam, Supercell, etc. — fall from grace.

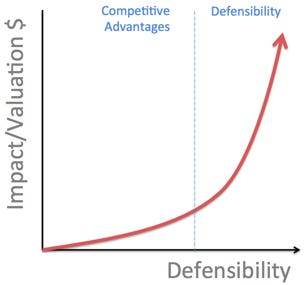

To give specific context to this discussion, a very useful framework to think about long term defensibility comes from the venture capital firm NFX. They have a number of great posts related to company defensibilities although they themselves prefer to focus on network effects (hence their name NFX) based companies.

I would argue that the vast majority of game companies sit on the left hand side of the NFX chart above: they may have strong competitive advantages but relatively weak (to other industries) defensibilities.

The purpose of this post is to think more critically about the longer term resiliency of game companies in our industry.

More specifically, this post explores the following key questions below:

Key Questions

#1. Current Strategies: What are the defensibility strategies of current game companies today?

#2. Defensibility: Can we conclude that the vast majority of game companies are relatively indefensible over the long term?

#3. What To Do: If game companies seek to be long lasting, durable, and resilient companies that survive for 100s of years and not just 20-30, what should game companies do?

1. Current Strategies

What are the defensibility strategies of current game companies today if not network effects?

NFX defines four “defensibilities”: the ability to maintain long-term positions of market leadership.

According to the investment firm:

“’Competitive advantages’ help your company become successful. ‘Defensibility’ helps you stay there.”

These are the four defensibilities from NFX with examples from tech:

Applied to the gaming industry (content companies), here is my own interpretation for the archetypal companies for each defensibility category:

So how defensible are game companies based on these defensibilities? Let’s investigate each defensibility below.

Economies of Scale

Unlike Amazon which owns massive infrastructure, technology, and purchase and store search data, economies of scale for game companies don’t provide as much of a defensive moat to their businesses.

However, generally speaking for game companies, scale does benefit in three primary ways:

#1. Capital

First, as a hits driven business, companies like Activision have access to capital that allows them to invest in big game projects that other companies cannot. Further, the more capital a game company has the more they can spend on marketing to achieve “launch velocity” for marketing campaigns. In the mobile free to play area, additional capital also means the ability to fund long payback games at scale (e.g., Match-3 or social casino often have payback windows on a 2+ year time horizon for example).

Note however that unlike Amazon, the scale of the barrier to achieve economies of scale occur at far less amounts of capital. Budgets for AAA console games could be more like $20M-$50M (notwithstanding Activision’s $200M+ budgets for Call of Duty although also including marketing and distribution). Further, with publishing program’s like Epic’s, even very expensive games can be funded through a publishing partner.

On the mobile side, development budgets are half or even much less than on HD (console + PC platforms) and a UA budget of even as little as $3M may be enough for the majority of mobile games to compete with bigger publishers. In some rare cases, mobile launch budgets can potentially exceed $50M.

Meanwhile, Amazon spends slightly over $11B *every year* on capital expenditures.

Between Amazon and Activision, I know who I’d rather compete against. Not saying it’s easy, but one scenario is possible while the other is just outright ludicrous.

#2. Leveraging Audience: Data and Cross-Promotion

Secondly, having access to players and player data from having launched other games can help in new game launches. Companies can not only cross-promote audiences from one game to the next, but player data from one game can be used for other games as well. For example, player purchase information from one game can be used to help target similar buyers in another game using Facebook “lookalike audiences.”

However, the magnitude of defensibility for having an existing audience have routinely been overcome in our industry. Even further, marketing on Facebook and Google is increasingly a more level playing fields as specific targeting and using lookalike audiences becomes less impactful in favor of broad based targeting. Therefore, while presenting some shorter term margin advantage, this has not been a significant enough defensibility to keep out new competitors.

#3. Size of Audience

Economies of scale can accrue both on the cost side and the revenue side. Epic’s Fortnite demonstrates a good example of leveraging economies of scale against its audience on the revenue side. While per player monetization is relatively low in Fortnite, the company can leverage its massive install base of users to justify very expensive IP integrations like Batman, Star Wars, etc. Further, the scale of audience in the game can also justify creating iconic in game experiences like the recent Travis Scott concert.

Fortnite’s continued decline and the ability of new entrants (e.g., Apex Legends, Call of Duty Mobile, etc.) to gain share, however, suggests this defensibility is limited.

Brand

Of the defensibilities defined by NFX, brand is likely the most commonly used by game companies. Supercell, Activision/Blizzard, Riot, and Nintendo don’t need to market their games as strongly as other game companies for the same distribution. EA deploys brand not only as a signal of quality for its games but also as the basis of its product strategy.

To help quantify some of this advantage at least on the F2P mobile side, I believe that while most mobile game companies may be spending 30%-40% of game bookings against marketing/user acquisition, a company like Supercell, based on the strength of its brand, could be spending 10% or less (based on my own rough assumptions).

When we look at the landscape of the biggest and most successful game content companies today, we see that brand is the most common defensibility. However, in games, we have seen once powerful brand-defensive companies like Atari and Rovio become a fraction of their former selves. Hence, clearly brand by itself is not enough to sustain long-term success.

Embedding

We see embedding defensibility more in game infrastructure and technology platform companies. Hence game engine companies like Epic with Unreal Engine or Unity play here. Further, we see companies like Facebook for game log-in, MMPs (mobile measurement partners), tools (e.g., Firebase), etc. use embedding strategies with game content companies as customers of their technology.

However, we have yet to see any examples of embedding for game content companies. Quite possibly a future opportunity if someone can figure this out, but currently this defensibility does not play strongly in gaming.

Network Effects

According to NFX, “network effects” are responsible for 70% of the value created by tech companies since the Internet from 1994.

NFX states even further that companies with network effects “end up creating the lion’s share of the value.”

When we think of game companies, however, almost no game companies have strong network effects based on the definition from NFX:

“Network effects are mechanisms in a product and business where every new user makes the product/service/experience more valuable to every other user.”

NFX lays out various kinds of network effects in more detail in this post.

Also, just to be clear, NFX has also posted on their company blog that they are “bullish” on gaming startups although at the same time being focused on investing in companies with network effects.

Based on the NFX framework, we can conclude that few game content companies have network effects. Three notable exceptions:

Roblox operates a 2-sided platform — a creator and player marketplace

Epic and Unity’s game engine business exhibits 2-sided platform network effects

AppLovin operates a 2-sided platform, its ad network, but for gaming, that platform could offer (no comment on whether they use their data in this way or not) asymptotic data network defensibility to inform user acquisition and product portfolio strategies

Strictly considering game content companies, however, we can conclude that few have network effects. If anything, Epic’s Fortnite and maybe games like Candy Crush or Call of Duty on the HD (PC + Console) side have network bandwagon effects, but overall these defensibilities are relatively weak.

For clarification, network bandwagon effects mean when a game becomes so popular that other people want to play the game to not be left out. Fortnite is a great example amongst teenagers where kids at school who constantly talk about Fortnite cause other teens to jump on.

You could also argue that some multiplayer PVP games have some notion of an “asymptotic marketplace” in that the more players that join those games, the better the game’s matchmaking, and the lower player wait times for a match will be. However, for the vast majority of game content companies, there are no or relatively weak network effects.

2. Defensibility

Can we conclude that the vast majority of game companies are relatively indefensible over the long term?

Facebook has a massive moat of network effects, Amazon has massive scale defensibility, but game companies today primarily rely on brand or scale defensibilities that are not nearly as strong. Hence, in gaming we have no company as powerful as Facebook or Amazon in their respective industries.

Of all the game companies, the only company I fully expect to survive 100 years from now, in 2120 based on defensibility, is Tencent. However, Tencent operates in a lot of other businesses that do have network effects and beyond that owns a piece of, or partners with, just about every major game company in the world. Hence, they are different in that they are not a pure play game content company and they are hedged by owning a large part of the entire industry.

Are there any other exceptions? Let’s look at the companies that have been around for a while.

Nintendo (founded in 1889)? Maybe Activision (founded in 1979)? Maybe EA (founded in 1982)?

All three are brand-defensive companies, and of these, both Nintendo and EA have, unfortunately, not been able to successfully navigate new game platform transitions — currently mobile gaming — as a dominant competitor. Activision has done better with its acquisition of King but interesting to note that there has been zero synergy between King and the rest of Activision. For mobile, the greater synergy for Activision was actually through the launch of Call of Duty Mobile with external partner Tencent and their famous TiMi Studio.

Despite their weaknesses (mobile and integrating acquired companies more synergistically), these companies do represent the more long-lasting and durable companies in our industry relative to others. Within these three companies, I would argue that Nintendo and Activision/Blizzard seem to have much stronger defensibility relative to EA. However, let’s get back to the rationale behind this later in this post.

In terms of other companies, Riot for example, while showing promise in finally launching other titles not named League of Legends, are still grappling with scaling beyond their first successful product. Fortunately, Riot is showing a lot of promise in new titles like Valorant. Hence, I wouldn’t count out Riot but, they still have to prove out longer term defensibility.

Are there any other exceptions? Let’s look at the mobile gaming companies

Of the public mobile pure play game companies, Zynga and Glu, both of these companies have yet to prove long-term economic viability. And while both companies have been on recent upswings, historically they have not shown an ability to show consistent profitability.

Note that while Zynga shows a recent upswing in free cash flow, in 2019 they recorded a $314M profit on a sale and leaseback transaction for the building they own — obviously not related to their core business. Glu also made one of the best acquisitions in the history of mobile gaming in 2016 with their $46M acquisition of Crowdstar and still struggles with profitability.

In either case, even this 5 year snapshot shows inconsistency in their ability to be economically viable over the long term… not to mention the full history of inconsistency which I leave as an exercise for the reader to investigate.

Of all the big mobile gaming companies (excluding China), perhaps Supercell has the strongest defensibility, but even they are in decline.

This underscores the point made earlier, but also for mobile gaming: there is no Amazon or Facebook in mobile gaming.

Are there any other exceptions? Let’s look at the companies with network effects.

Earlier in this post, I mentioned 3 gaming companies that have network effects:

Roblox

Epic

AppLovin

Roblox

Roblox does have strong network effects driven defensibility. There’s certainly a reason Roblox has managed consistent and steady growth and continues to not only dominate on PC and console but also on mobile platforms as well.

In mobile Roblox is regularly in the Top 10 Grossing charts (based on SensorTower):

Clearly, Roblox has benefited from network effects defensibility despite focusing on a traditionally very difficult market to monetize: kids.

For pure play game content companies, however, this type of defensibility won’t apply. Hence, while Roblox has a fantastic business as a game content and infrastructure platform, the lessons for game content companies is limited.

Epic

Epic is another company that while declining in defensibility as a game content company has increasing defensibility as a game engine company. Further, it’s pretty clear this is one of the few companies thinking strategically about how they will build defensibility in the future. The bold types of experiments they are running in Fortnite, recent moves to gain share for their engine, and opening up their online services, are examples of a company focused on expansion and longer term defensibility.

AppLovin

Perhaps the one other company to consider with respect to defensibility is Applovin which has an asymptotic data network effect. The data that they collect from the ad network side of their business they could potentially use (rumored) to inform the game development side of their business.

The commonality in this area between Epic and Applovin are that both companies explore vertical and horizontal integration outside of just game content.

3. What to Do?

If game companies seek to be long lasting, durable, and resilient companies that survive for 100s of years and not just 20–30, what should game companies do?

Relying on brand is not enough. Scale defensibility is limited in our industry.

Yet these two pillars of defensibility in gaming are the most common.

I believe there are 3 nuanced defensibilities that game companies should build to create long lasting, more durable, and more resilient companies in the future.

#1. Brand/Original IP

Previously, I mentioned Nintendo and Activision/Blizzard as the two companies having the greatest defensibility in gaming (well besides Tencent).

What are the commonalities between these two companies and different from the other companies that aren’t as defensible?

Both companies are brand-defensive, but I would add a more specific sub-categorization of brand defensibility which is the strength of their IP. Warcraft, Starcraft, Diablo, Call of Duty are incredibly powerful assets that players want to identify with, can be deployed to generate additional product SKUs across different game genres, lower cost of marketing, reduce design and production time, and can be deployed on new gaming platforms such as mobile to extremely powerful effect.

The power of characters, story, and emotion through IP owned by gaming companies should not be overlooked. Game companies should be investing in original IP rather than giving away not only margin but longer term company defensibility.

In this regard, some of the best companies here include Activision/Blizzard, Nintendo, Riot, and Supercell as key examples.

#2. Organizational Advantage

Of the mobile game companies, I mentioned Supercell having the greatest defensibility. They not only have fantastic “Clash” IP, but in my opinion a defensibility not discussed by NFX: organizational advantage.

Supercell focuses on small teams, does not pressure short term thinking, focuses on quality, and are structured in a way to enable the company to have a better chance of making big hit new games rather than just incrementally optimizing games. They started off with a big advantage in terms of having a decentralized “cell” structure which it turns out is superior to centralized forms of organization due to the requirement for specialization, genre expertise, and increasing depth over “pattern recognition.”

In my experience, some of the biggest companies with massive resources actually are the most likely to fail in games. Poor leadership, bloated organizations, focusing on the wrong priorities, and toxic cultures lead to failed products. Therefore, the organization and the culture of a company can be an incredible defensive moat if everyone else is unable to adapt accordingly, due to politics, culture, and inflexibility.

In practical reality, very few companies can be like Bridgewater, Amazon, and Tesla culturally. In fact, people change slowly if at all. Hence, creating an organization that can promote change in people can be a significant advantage.

Just to be clear, however, while Supercell has very distinct advantages relative to competitors, they still have a ways to go.

Organizationally, the other areas Supercell has left to improve include (based on speculation and what little I know of the company):

Organizational Improvement: Becoming more of a learning organization

Global Organization: Understanding how to expand as a global organization (not just random minority investments in a haphazard way), but to actually become a global rather than Finnish organization

Best Practices: Increasing focus on best practices and understanding how to incorporate some level of centralized advantage to their decentralized structure

#3. Scale/Technology Infrastructure

Finally, the last defensibility is a type of scale defensibility.

What can we learn from the most valuable company in the world?

Today, that company with a market capitalization of $1.3T (6/11/2020), is Amazon.

Amazon invests, for the long term, in infrastructure: warehouses, automation technology, logistics technology, machine learning based recommendation systems, cloud infrastructure, etc. The infrastructure Amazon has built creates the massive and now insurmountable moat for new entrants.

Gaming today is increasingly shifting to live operating models due to the explosion of free to play monetization. The knock-on effect of a live operating model is the requirement for continuous and on-going optimization and marketing.

I wrote here about how live ops is the next frontier in game infrastructure services. Hence, understanding what to build and how to deploy a game company’s live operating technology infrastructure will be one of the most significant defensibilities and likely the one most of the PC and console guys will have the biggest difficulty in executing against.

In Conclusion

While we currently don’t have an Amazon of gaming, I believe that game companies can build long-term, durable, and resilient businesses.

But just to be clear, we aren’t there today… Sure maybe Tencent. Of non pure play game content companies maybe Epic or Roblox.

Having said that, I personally welcome the challenge of thinking critically about how game companies can build defensibility that lasts. What do you think? Let me know in the comments below!